Miftah Ismail Ahmad, Minister of the State for Finance, who also presented PMLN’s past Government’s Last year’s budget in the absence of Ishaq Dar is the rightful owner of the Candyland company which made my childhood a Dream. If you are a 90’s Kid, have you ever sang along with the advert jingle: “Abhi lao abhi khao; Candyland ki Chocolate Now”. Well, I for the one always did and took the Chocolate “Now” as part of my lunch for the school. Miftah Ismail remained a Pakistan Muslim League (Nawaz) candidate from NA 244. He contested for the first time against Ali Zaidi from Pakistan Tehreek e Insaaf, Ali Raza Abidi of Pakistan People Party, and Zahid Saeed of Jamat e Islami.

The candidature split of KHI Election 2018 about the constituency of NA 244:

- TLP. Syed Jilan Shah

- PTI. Ali Zaidi

- PPP. Saeed Ghani

- PML N. Miftah Ismail

- MMA. Zahid Saeed

- MQM. Rauf Siddiqui

The Start of Miftah’s Political Campaign:

Miftah Ismail’s family background also supports his candidature. He is a memon. He is Sunni-Barelvi. He is monetarily rich. To the advantage of Miftah, he and his entire family are from KCCI and FPCCI. All the Memon community also supports him. There had been an online Twitter trend #MiftahForKarachi. He has also met, Dawat e Islami, Nigran e Shura Haji Imran, Haji Amin, Abdul Habib also. Shiekh Tareeqat performed Tauba Bait and Dua for his success.

Miftah Ismail has done much to promote business related activities in Karachi including law & order control and load sheddingMunawar Younus

Miftah had done a door-to-door campaign in NA 244 as it is a constituency of the Dhoraji Memon majority. His agenda drives through the massive business development projects and new opportunities for Karachi, securing the rights of individuals & ensuring them with an uninterrupted supply of basic facilities i.e. water, electricity, and gas. He is very courteous, and I learned through my interaction with him that I misspelled his name and he did not mind.

Something on Miftah Ismail’s Career

I got myself acquainted with him as an influencer while I was doing my internship with SLB or Schlumberger. I was reading his article in Dawn Newspaper. Those were Ramadans of July-August 2012 and we had the liberty of taking extra-long breaks. Anyways it was a 2-minute read. And man! I was flabbergasted that PMLN had such minds. So composed in thought and youthful. Although, elections had not yet taken place but reading his impressive remarks on the then KSE, and now PSX, gave me good vibes about this person. That he soon could participate in the electoral from Karachi.

Something on Miftah Ismail’s Educational Background is really interesting. Dr. Miftah Ismail Ahmad, who is a Bachelor of Science from Duquesne University in Pittsburgh, PA, and Studied at the University of Pennsylvania, later did his Ph.D. from The Wharton School, Philadelphia, PA. His discipline majors in Public Finance and Political Economy. Miftah remained as an Economist at International Monetary Fund from August 1992 till May 1993. A decade later, he acted as Vice Chairman Punjab Board of Investment & Trade (PBIT) from Jan 2012 – to Dec 2012. He also served as Director of Pakistan International Airlines for seven months starting from Oct 2013 and lasting till Jun 2014. He also has experience of remaining as Director of Sui Southern Gas Company from Oct 2013 onwards.

Beggars can’t be choosers

Later, in August 2014, two years after I contacted him via LinkedIn to give me a job in his organization. He politely responded and asked me to supply my CV. Which I did! On merit, I was rejected. He did not give me a job! On a serious note: this adds to the sincere contribution he has made at Candyland being the Directors for being honest and courteous at the same time.

As per industry experts, Dar and later on Miftah had hedged the dollar value for a long. This increase was due and much expected. This is the only truth he brushed into your face and accept last time and now.

Mujh se behtar koi nahi janta web 3.0 ko

If you ask Imran Khan about it. Actually, the appropriate answer would be: “Web 3.0 ko mujhse behtar koi nahi janta”. I will still neither call Mr. Imran nor current PM Jahil because neither they nor their finance ministers have anything to do with web 3.0. And if someone doesn’t know something it doesn’t make it a clown. But I have a fair idea, Imran couldn’t know it because he doesn’t know anything beyond foreign conspiracy nowadays. Previously he use to talk about quantitative objectives, like 5 million homes or 10 million Jobs, as he has learned that he cannot possibly achieve it in the next 50 years he is selling abstract objectives. Like khudari and self-reliance which no one can measure and hold him accountable for!

There are no web 3 experts in the world because literally, no one knows what it is. Muhammad Omar Nasir – A Fintech Expert

Explaining Web 3.0, this is generally what Mr. Omar Nasir had to say:

- So in the ongoing cycle of the web, clients are the item that implies the stages are free (Google, FB) and you have zero commands over your information. Your movement on the web is adapted, however, you get no part of the income.

- Web3 proposition is to guarantee all administrations are somewhat client claimed, and when you play out some movement on a stage you fundamentally get compensated in crypto coins. That takes care of the adaptation issue and creates income for both the client and the stage (if the crypto cost goes up). Is there something more than monetization to it? like Social Media banks? Or exchange of clout like Klout or Kred? (Exchange like for like?) For the time. No. It is just monetization.

- Another more treacherous application is making the client pay crypto tokens to get help. You can get too specific elements on stages provided that you purchase those coins and spend them on the stage. For example, if you need to post a status update on web3 FB, you need to spend crypto tokens. You can also probably earn crypto tokens on the same platform by engaging in other activities. This will only serve to make your internet experience completely miserable. Omar believes the concept would be that you need to spend tokens to upload a video and then other people need to pay to watch it, thereby generating revenue. Not sure how TikTok would work in web3.

- What makes all of this staggeringly moronic is that it professes to remove the power from focal specialists (like FB, yet it’s clearly false) and give it to the client, yet there is just no restriction to the number of coins an individual can possess. You will without a doubt wind up experiencing the same thing as a couple of rich people who will support every one of the coins and have unlimited authority over the stage. It settles the score more regrettable: crypto can be made difficult to follow so essentially some obscure very rich ppl will assume command of significant administrations with no guidelines set up.

- Is NFT and Fintech part of it? NFT, yes. Fintech is just a term. You could apply it to web3 monetization. Or not.

- Does this mean employing people to engage with content to earn coins and in return being paid a small portion in terms of the real money? This is about DAOs, a form of user ownership in which people who own the tokens behind a service get to make decisions. Trouble is, that a single person can own majority tokens and abuse the voting system. there was a recent $180m hack based on this exact same flaw.

The hacker loaned themselves a lot of crypto tokens, enough to give them control over the company. They then voted to allow themselves to take control over all the tokens, thereby giving themselves free money.

- So to finish up, it’s a very crappy thought that just reformats the current issues of the web into another worldview with not so much oversight but rather more open doors for misuse.

Social Media Banks

With the accumulation of funds owned very large, perhaps only Google, Amazon, Facebook spread its wings into a bank, at least has a subsidiary specialized in banking that can support their business expansion. Globally, some people assume that the World is not in position to have one currency, walls are already there. Bitcoins have very little recognition. Euro has problems too. According to these people times are not ripe for global bank. But the future is all about tech. Therefore, the technology giants are going to dominate the financial landscape. Facebook just secured an e-money licence from the Central Bank of Ireland too in Dec 2016 that is. It will change everything from financial services companies going bust to banks closing down because big data is now more centralized with Facebook and Google. These corporations are almost certain to offer banking services in the near future. Personally, we think Apple has the best chance of being first and successful.

Anyone who says ‘privacy is overrated’ shouldn’t be taken seriously

Blockchain technologies offer up some huge potential in these areas to create new models that move profit margins from the big organisations to customers pockets. Regina went to FB for one big reason. That is centralization. In lots of ways it is singularity in motion. Facebook knows you better than your bank does. Doesn’t that mean that our information will be stored in other countries, from our understanding Google and Facebook will have to keep our information in Australia so how secure is that when these companies are global? We see it as a failure. Regina Dugan will have everyone eating their RFID passchip before you know it. Her DARPA background is perfect at her new home with Facebook! Bankbook! In Spain, Facebook has begun few days ago as financial company registered in Spanish Bank.

It’s not Scary, it’s just New

Client trends are changing and it is not a surprise that banks in the traditional sense need to reinvent themselves. There is really no need to have large banking offices, clients are using other methods to perform all their banking transactions. Google would be a good platform to run financial products, will Google become a bank? Not sure. However they have the technology and the client experience to launch a new idea of banking. The banks of the future do not required Debit or credit cards, you will paid with your phones or your finger print. We believe that Google has the human talent to be able to develop a more sound financial system to prevent fraud and detect unnecessary financial fees on the spot. The idea of thinking that clients need an office at every corner is obsolete. It is important that banks adapt quickly to the changes and think about the future. The future is going towards a cashless banking industry where one platform manages your home, your office, your finances and your personal life.

Google bank is coming soon! We’ve been listenting this will occur for last 10 yrs. They are already entering (or have already entered) the payments space look for example the Google Merchant Account. Bank’s are so far behind the technology curve there is effectively no real way for them to catch up….only differentiate. EMMAR can associate Google banking. If Alphabet wanted to buy a bank, really….what would stop them?? After all, the systems are just being switched to fully online. (Rather than a physical place) Could this be the first line in the horizon for more commercial usage of Bitcoin? Why become banks, when you can become the ultimate authority. If you have a problem, just ask google. If you need something just ask Amazon, if you want to talk to someone, just go on Facebook. It’s not like communication existed before these companies. Why not have these corporations take over the world? There would be no unemployment.

No Place for Conventional Banking in Future

What is the last innovation you remember a bank providing in terms of value to you? Internet banking? Now that’s a bit embarrassing isn’t it. As for Google and Facebook, they’re both social Networks. Networks like these 2 companies would gamble with your money and lose it all. Since banks don’t like losing money and are made up of people’s money, they also have no business becoming banks, especially Facebook. These corporations have more connect to people than banks do. Banks are hierarchical and non responsive to many general needs. Banks have to reinvent and even though it may or may not be good to have these companies now entering a potential banking space, its good compete and gives something for the banks to work on. To be honest, we really think that they already are … But they wont build “walls”. We believe these Social Media banks will choose selling more lucrative products and processes. These services will be convenient, cross channel and efficient. Existing banks will have a terrible time to compete. Credit unions ARE banks. Many insurance companies are banks (State Farm, AAA, etc.) So banks growing out of a “membership” such as Amazon and Facebook are actually more like the original CUs!!! They don’t have to be a traditional bank, maybe they add some much needed legitimacy to bitcoin by joining up with other tech companies to support it.

The Answer is Yes and No

Yes they will operate banking services, probably through a partnership with either an established bank or the best of the start ups. The reason they wont become a bank (established themselves) is due to the regulation that’s involved. Google and specifically Apple want to own the front end experience, due to the marketing opportunity, and the potential to deepen the relationship with the customer. We cannot imagine both companies wanting to clear money and manage accounting based reporting. The real player that could make the biggest impact is Amazon. With links to a market place, and now in our home due to echo, they have huge reach. We see two possibilities in the next 2 years. Either a bank will be bought and staff retained, or as stated a partnership with a bank. Either way the tech giants will start to own more and more front end banking services until banking becomes invisible to us.

If the American people ever allow private banks to control the issue of their currency, first by inflation, then by deflation, the banks and corporations that will grow up around them will deprive the people of all property until their children wake up homeless on the continent their Fathers conquered…. I believe that banking institutions are more dangerous to our liberties than standing armies…. The issuing power should be taken from the banks and restored to the people, to whom it properly belongs.

-Thomas Jefferson

Why do you say that social media is a free ecosystem? It is not “free” you just don’t pay with money and they all sell your data. The big corporate attached to these social platforms are the true Internet trolls! There are definitely a lot of complexities when it comes to banking and these tech companies taking over. This would obviously create disturbances with privacy issues, in which Americans value privacy heavily. Also, it would promote monopolies in many facets. This destroys the idea of fair markets and competitive, capitalistic ideology. We are truly unsure about this without getting into more depth but all in all, we believe that would be a horrible move for the tech companies and we also believe it would be a horrible move for citizens. Internationally, this could be effective.

Modus Operandi

First, they would have to be granted a banking license. Secondly, they would have to be regulated the way a bank is regulated. In a less regulated market though it could happen. Large technology companies as those mentioned upto this stage of the article will likely be better served to own a bank holding company, or partner with one that can carry the regulatory and infrastructure burdens while allowing the tech firms to expand services through their existing channels without the unnecessary weight of additional regulatory expertise. This can be compared to companies either owning their own property or leasing from a specialized company that owns and manages properties. If ownership is in your capital structure interest, then do it, but if it isn’t, let someone else own it so you can put your capital into what you’re good at. If Nuon is a bank, we are sure Google already is.

Time to bring back Glass-Steagall

Isn’t Microsoft vested in the same “technologies”? Interesting to see that a LinkedIn Editor would leave them out of the whole scheme of things, especially following Microsoft’s acquisition of LinkedIn. Perhaps a way of making Amazon/Facebook/Google “too big to fail”??…smells to high hell!! Commercial banks are not supposed to be high-risk ventures; they are supposed to manage other people’s money very conservatively. It is with this understanding that the government agrees to pick up the tab should they fail. Investment banks, on the other hand, have traditionally managed rich people’s money — people who can take bigger risks in order to get bigger returns… oligarchic deep state writ large… what a disgrace…

Wiki: Glass-Steagall Act

The plaque at the old Shakey’s pizza parlor said it all,

“Shakey’s doesn’t cash checks, the bank doesn’t make pizza.”

Owning the technology infrastructure and the “user experience” is extremely lucrative. On the other side, being a bank can be lucrative but it also requires that you maintain much of the “plumbing” of the banking process which is a) very cumbersome, b) heavily regulated, and c) becoming commoditized.

Editorial Word on Social Media Banks

The Lord would have us understand that no one’s spiritual lot can be improved by being a lender or a money changer. Overall Social Media Banks are disguised as advertisements, but it is Big Data that sells your confidential assets, emails, IP address & other very confidential information to other corporations. Facebook’s database should be printing its own dollar anytime soon. In large, big companies will play it safe with new concepts, especially with old institutions like banks. The big 4 (Google, Amazon, Facebook, and Microsoft) will stay in their respective lanes as a long-term approach and might dabble in a few financial projects in the future. We would rather suggest – banks should become Google, Amazon, etc. by embracing technology and providing the next generation customer satisfaction and user experience consumers. If you stop and think about all the disruption (think of the UBERs of the world etc) it is all orienting value around the customer using new models and technology. We don’t see why the archaic bank models would be any different, as contrary to pointed out above, it may just take longer to gain trust. In the end, we Pakistanis had always listened to the notion that Israel controls the World Online economy. The plastic money is a hoax. Here you go, guys. The real New World Order.

Recent Criticism Tirade on the Cocomo Man

Boycott of all Candyland products is the talk of the town. Cult followers are going to defile anyone that doesn’t belong to their favorite party. They were too blind to see anything when the last government changed finance ministers like diapers. Some people are labeling someone a clown if they don’t know about web 3.0. They say, he is supposed to know this, he’s the minister of finance, he is representing financial policies, and he’s accountable for it all. He is the policymaker of a country that has immense IT export and resource potential.

I would say, ask Miftah about macroeconomics and then judge him. He has a Ph.D. in finance, not in technology. Even many technologists are bewildered about this. If he would’ve uttered nonsense about web 3.0, he would have received more harsh criticism for distorting facts. Everyone is disregarding the most important thing and that is he said the government won’t intervene over there. That’s the spirit Pakistan has been waiting for years. Let’s just hire a web 3.0 expert (are there any) as the finance minister. Sab theek ho jae ga?

People draw wrong parallels here. If you want to compare, compare Ahsan Iqbal with Murad Saeed, compare Hina Rabbani with Shah Mehmood. Sania Nishter was given the portfolio of PTIB first and she replaced Dr. Umar Saif. If you want to compare, Compare Sania with Dr. Umar (whom I clearly don’t like). Even Mr. Miftah Ismail is a very seasoned Economist. Read him and listen to him beyond the myopic vision. Much better than the likes of Asad Umer. No issues that’s why there are advisors who guide ministers about it.

Ph.D. in economics doesn’t equate to a multi-discipline grip over other matters. Better to acknowledge your limited understanding of the matter than claiming to be a master of the subject. He has particularly answered the question on web3.0, not on digital or cryptocurrency. Listen again. And in the last, he set out the policy guidelines that govt would not interfere in its development. This is how tech has evolved over the years. Plus, even IT experts are not agreed on one definition of such rapidly evolving fields. But yes, it’s Pakistan and you can claim to know this stuff & bash your minister after trading in Doge coins & Shiba.

He gave the perfect reply as a state representative over here. He passed the discussion to the state bank guy since they are more experts on Monetary things. Moreover, his reply is what we wanted that if you aren’t aware of something, we will not intervene over there. There are thousands of markets in different economies where the lawmakers have no clue about it, but they don’t interfere, unlike Pakistan.

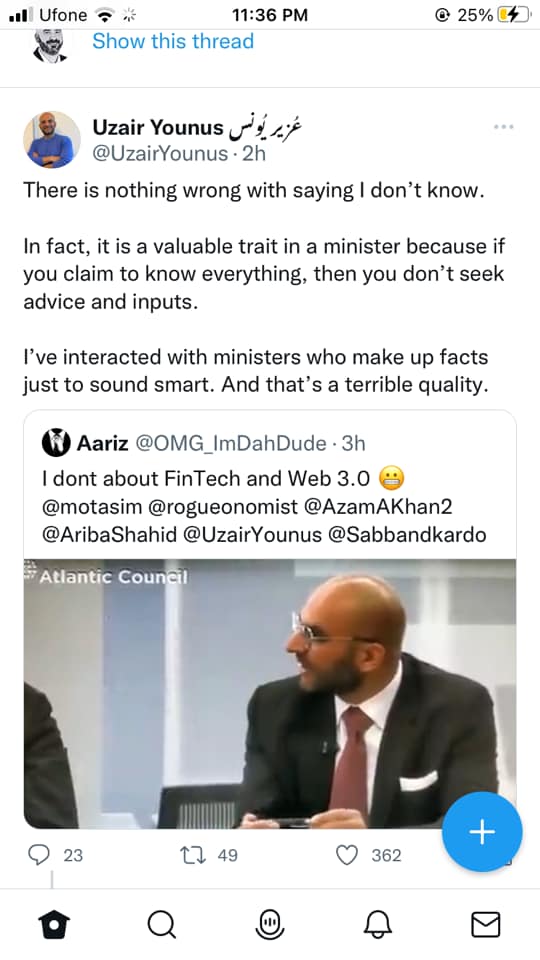

This is the take of Uzair Younus, the guy who asked this question to Miftah.

But no, we love to twist videos because of our grudge. How can he understand when the web3.0 industry itself hasn’t figured out yet what they are. The main point is ‘as long as government stays away from them, they are fine. Appreciate this that at least we are realizing government shouldn’t intervene everywhere. He claimed he doesn’t know much and we should appreciate that. Unlike Mr. Know-it-All the Imran Khan.

To the concern that he criticized IK for being too ‘Islamic’ at that forum. What does he want to achieve by doing so: portraying himself as a Liberal slave and portraying his political rival as an Islamic extremist? Well actually, he is not ridiculing a basic Islamic concept, he is ridiculing PTI’s cynical use of a Quranic verse to paint your political opponents as the embodiment of Vice. And Shireen Mazari’s response to this is identical to rightwing parties that paint all criticism of them as attacks on Islam. This is the use of religion and that’s what IK violently opposed and had similar thoughts on Maulana Fazl ur Rehman. Now, if his opponents are accusing him of this, why feel offended?

Rest as for IK that’s totally his own opinion and he also has the right to freely express his opinion as amar bil maroof wa nahi anil munkar means “enjoin what is good and approved, and forbid what is evil and disapproved”, this is completely based on the people who have to decide what is good and wrong for them

Don’t know about his performance but definitely a finance minister we needed. Finally seeing someone coming from the background of economics, instead of accounting/MBA/finance people. I like the fact he is democratic and engages with economists who don’t belong to any party. Furthermore, this guy listens to the opinion of different economists on Twitter and is humbled enough to take the opinions of twitter economists. Recently he had a discussion with everyone on ProfitPk.

Finally, Miftah who is the current “bloody finance minister” or Federal Minister for Finance, Revenue, and Economic Affairs at the Government of Pakistan, could be reached at: miftah.ismail@candyland1.com unlike PTI ministers where you educate them on something and boom, they raid your social media and murder the stats. He has the guts to listen and respond.